Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The following analysis of the Big Island real estate market is provided by Windermere Real Estate Chief Economist Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact me.

ECONOMIC OVERVIEW

Hawaii’s economy offered a mixed bag of growth in the fourth quarter of 2018. Employment declined 1.4% but the unemployment rate was a healthy 2.3%. Year-over-year, the economy has shed 9,300 jobs, and annual job gains have been negative for the past three months.

On the Big Island, employment growth dropped 2.6% and has been negative for the past five months. That said, there are 85,800 persons employed. The unemployment rate was 2.9%, up from 2.0% a year ago. The market has seen a drop in its civilian workforce since last summer, which may be artificially keeping the unemployment rate low, and there are over 3,000 job openings on the Big Island. At the present time, I am not overly concerned by the contraction in employment.

HOME SALES ACTIVITY

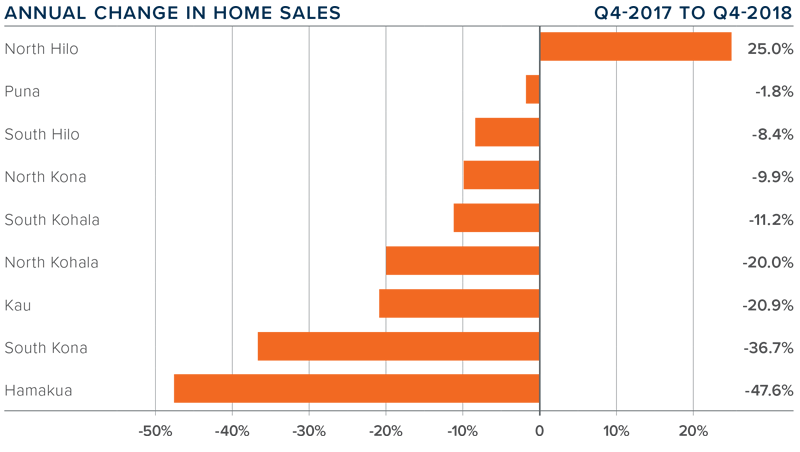

- In the fourth quarter of 2018, 742 homes sold, a drop of 10.4% compared to the last quarter of 2017.

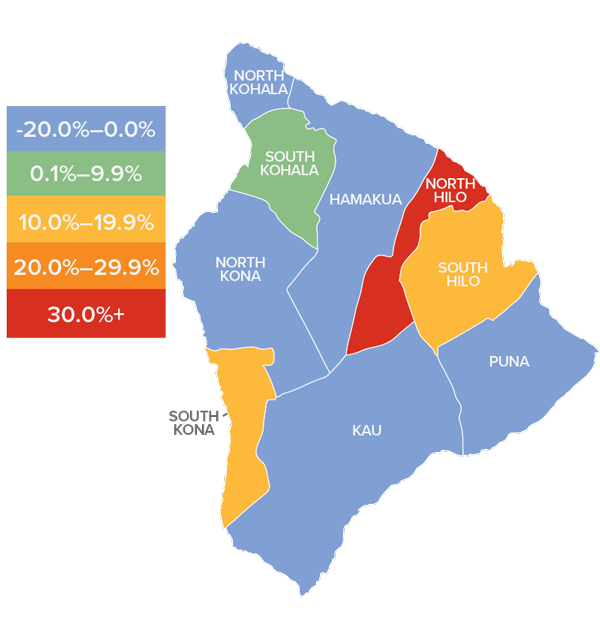

- The only market that saw growth in sales was North Hilo, which rose by a very significant 25%. But this is a small market and prone to rapid sales and velocity swings. There was a significant decline in sales in Hamakua but it too is a relatively small market.

- Interestingly, this decrease in sales came as inventory levels rose 4.8%. It is possible that this is due to the 2018 volcanic eruption. I will be looking at the data as we move through 2019 to see if this is the case or if there are other reasons for the contraction.

- Inventory growth continues to give buyers more choice and they continue to be far more selective — and patient — in making an offer on a home. That said, well-positioned and well-priced homes are still selling relatively quickly.

HOME PRICES

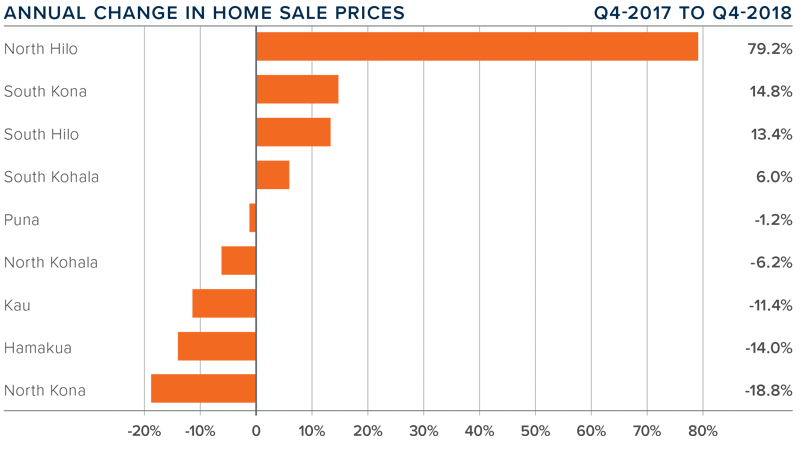

- The average home price in the region dropped 8% year-over-year to $527,997.

- Affordability is clearly becoming an issue, but the drop in interest rates at the end of 2018 may stimulate buyers. I will be watching the numbers in the first and second quarters closely to see if we experience a turnaround in price growth.

- Appreciation was strongest in the North Hilo market, where prices rose by 79% — again, a function of it being a very small area with limited sales. Four areas saw prices rise between the fourth quarter of 2017 and the final quarter of 2018, and five markets saw average sale prices drop.

- Because of affordability issues in many Big Island market areas, I anticipate we will see home prices rise in 2019, but the rate of growth will be modest.

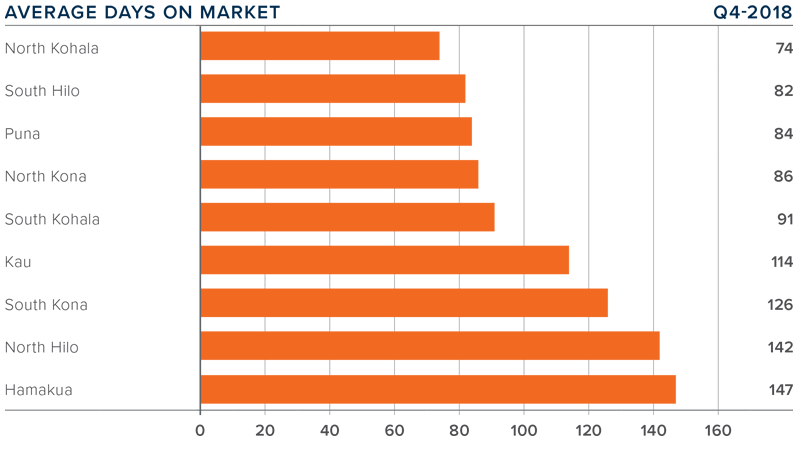

DAYS ON MARKET

- The average number of days it took to sell a home on the Big Island rose two days compared to the final quarter of 2017.

- The amount of time it took to sell a home dropped in six markets: South Hilo, Kau, North and South Kohala, and North and South Kona. The rest of the markets in this report saw days on market rise.

- In the fourth quarter of 2018, it took an average of 105 days to sell a home. The fastest moving market was in North Kohala and the slowest was Hamakua.

- Housing demand is still there, but buyers are clearly taking a breather. I anticipate we will see more activity and rising sales as we move through 2019.

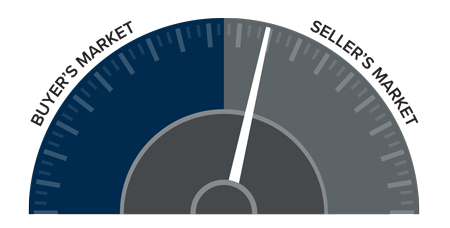

CONCLUSIONS

The speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors.

For the fourth quarter of 2018, I have placed the needle close to the middle. Although we saw a drop in sales and prices versus the fourth quarter of 2017, prices rose when comparing the whole of 2017 with 2018. I will be closely watching listing activity to see if we get any major bumps as we move through the first half of the year. I remain positive about the longer-term outlook for home prices on the Big Island.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governor's Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

")