Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

ECONOMIC OVERVIEW

The markets covered by this report, which include Los Angeles, San Diego, San Bernardino, Orange, and Riverside Counties, added 279,600 new jobs between November 2015 and November 2016. With this shift toward “full employment”, the area’s unemployment rate dropped from 5.5% to 4.7%.

HOME SALES ACTIVITY

- There were a total of 46,075 home sales in the fourth quarter of 2016. This was 7.9% higher than the same period in 2015, but 12.3% lower than the third quarter of 2016. This can be attributed to a seasonal drop as we wound the year down.

- The average number of homes for sale remains well below that seen a year ago (-6.8%), but the drop in listings is not as substantial as we have seen in the past.

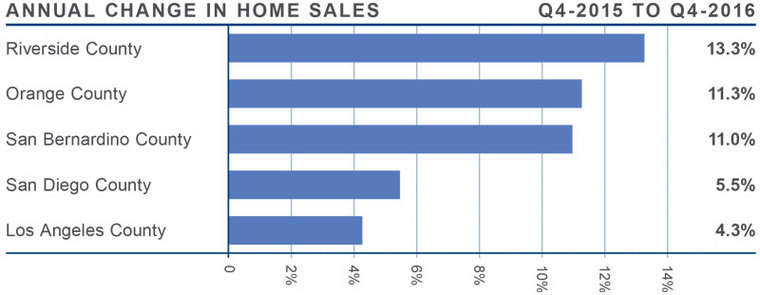

- Home sales were up across the board with substantially higher home sales in Riverside, Orange, and San Bernardino Counties. Reasonable growth was also seen in San Diego and Los Angeles Counties.

- Even with a relatively slim difference in the number of homes for sale compared to a year ago, we are still in need of inventory. We should see a minor increase in listings in 2017, but it is unlikely that the market will return to being balanced in the foreseeable future.HOME PRICES

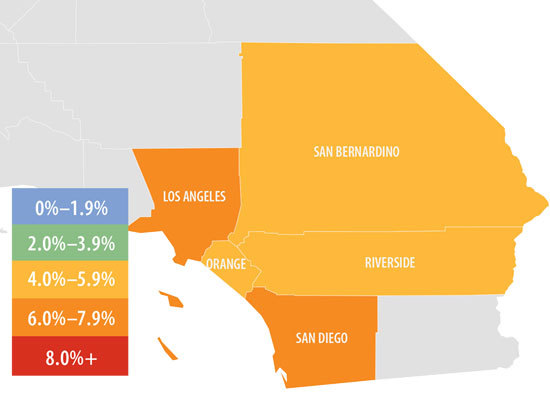

- When compared to the fourth quarter of 2015, average prices in the region rose by 5.9% and are 2.6% higher than the third quarter of 2016.

- When comparing the third and fourth quarters, all markets saw average prices rise, including San Diego County, where the average price rose by 5.4% to $634,300.

- San Diego County saw the greatest annual appreciation in home values (+7.8%). This was followed by Los Angeles County, where the average price rose 6.0% year-over-year.

- Pending sales were also higher across the board which, when combined with lower listings, means the market is clearly out of balance.

HOME PRICES

HOME PRICES

- When compared to the fourth quarter of 2015, average prices in the region rose by 5.9% and are 2.6% higher than the third quarter of 2016.

- When comparing the third and fourth quarters, all markets saw average prices rise, including San Diego County, where the average price rose by 5.4% to $634,300.

- San Diego County saw the greatest annual appreciation in home values (+7.8%). This was followed by Los Angeles County, where the average price rose 6.0% year-over-year.

- Pending sales were also higher across the board which, when combined with lower listings, means the market is clearly out of balance.

DAYS ON MARKET

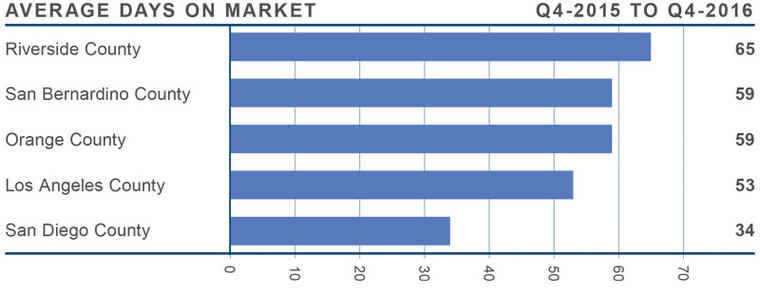

- The average time it took to sell a home in the region was 54 days. This is a drop of 10 days when compared to the fourth quarter of 2015, and one day below the time it took in the third quarter of 2016.

- The biggest decline in days on market was seen in Riverside and Orange Counties, where it took 14 fewer days to sell a home compared to a year ago.

- Homes in San Diego County continue to sell at a faster rate than the other markets in the region. In the fourth quarter, it took an average of 34 days to sell a home, which is five days less than seen a year ago.

- All five counties saw a drop in the amount of time it took to sell a home between the fourth quarter of 2015 and the fourth quarter of 2016.

CONCLUSIONS

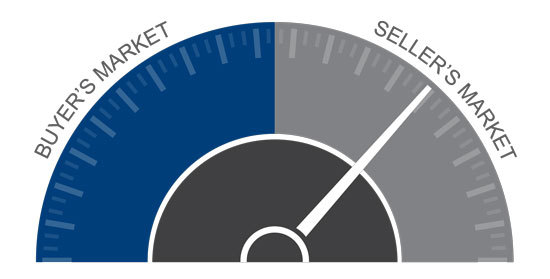

The speedometer reflects the state of the region’s housing market using housing inventory, price gains, sales velocities, interest rates and larger economic factors. The Southern California economy continues to add jobs, which in turn increases demand for housing. The region remains a seller’s market; however, it will be interesting to see what effect the recent rise in interest rates will have on the growth of home prices, especially in the more expensive Orange County and Los Angeles County areas. Given further anticipated increases in interest rates, I have moved the speedometer a little more in favor of buyers, but it still remains a seller’s market.

The speedometer reflects the state of the region’s housing market using housing inventory, price gains, sales velocities, interest rates and larger economic factors. The Southern California economy continues to add jobs, which in turn increases demand for housing. The region remains a seller’s market; however, it will be interesting to see what effect the recent rise in interest rates will have on the growth of home prices, especially in the more expensive Orange County and Los Angeles County areas. Given further anticipated increases in interest rates, I have moved the speedometer a little more in favor of buyers, but it still remains a seller’s market.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

Matthew Gardner is the Chief Economist for Windermere Real Estate, specializing in residential market analysis, commercial/industrial market analysis, financial analysis, and land use and regional economics. He is the former Principal of Gardner Economics, and has over 25 years of professional experience both in the U.S. and U.K.

")